“If you remain calm in the midst of great chaos, it will eventually subside.” Julie Andrews

People often describe how complex systems function using the analogy of a swan. Above the water, it glides along effortlessly—calm, composed, and elegant. Beneath the surface, however, its feet are kicking furiously in all directions, a hidden chaos driving that smooth motion.

Today’s markets feel like the exact opposite.

At first glance, everything appears unsettled. Headlines are dominated by geopolitical tensions—from Ukraine to the Middle East—along with concerns about cracks forming in private credit and growing skepticism around the scale and sustainability of AI-related investment. The narrative is noisy, uncertain, and at times, outright unsettling.

Yet beneath the surface, the underlying fundamentals remain relatively steady.

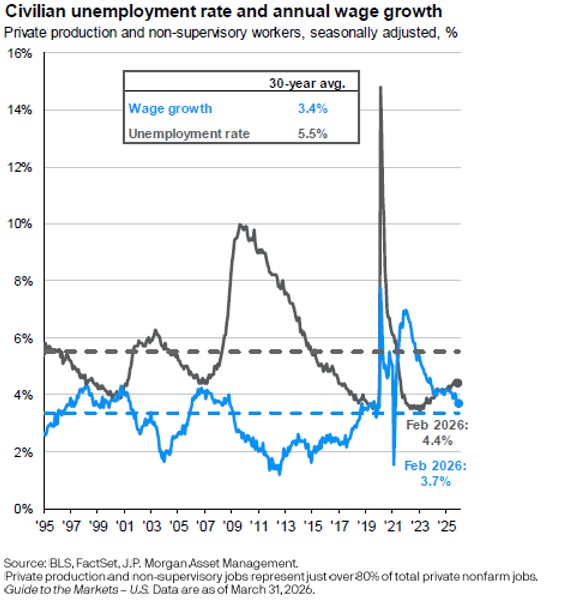

The labor market, while showing signs of cooling, remains healthy with unemployment still low by historical standards at 3.7% as of early 2026.

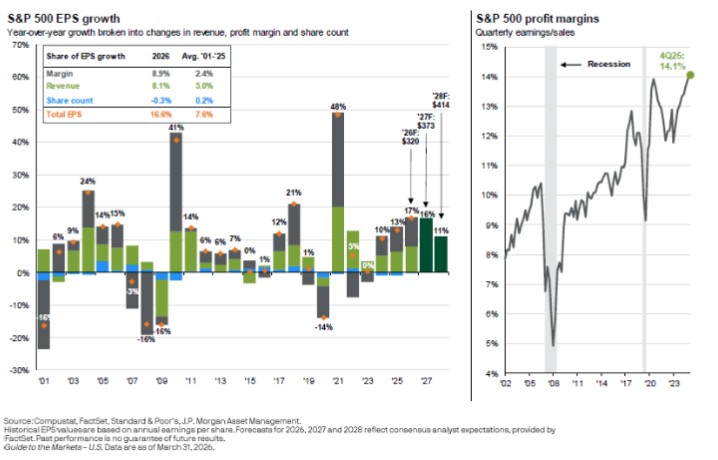

Corporate earnings, perhaps most importantly, continue to grow at a solid pace, with S&P 500 earnings expected to reach approximately $320 in 2026, representing double-digit growth driven by both revenue expansion and stable margins.

This helps explain the seemingly counterintuitive outcome for the quarter: despite the volume of negative headlines and some sectors of the market being down, portfolios as a whole were relatively unchanged.

This helps explain the seemingly counterintuitive outcome for the quarter: despite the volume of negative headlines and some sectors of the market being down, portfolios as a whole were relatively unchanged.

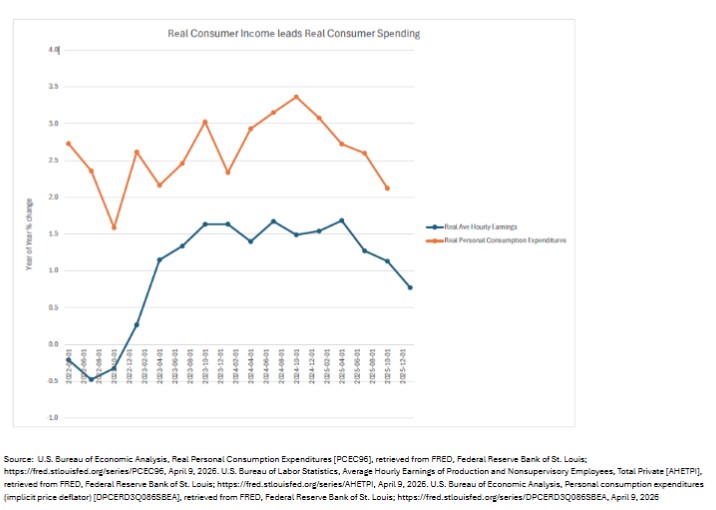

The one area that we are keeping our eye on is consumer spending. Real consumer spending has held up well recently and has grown at well over 2.5% over the last three years. If inflation remains elevated, it could reduce consumers’ real incomes and lead to lower consumer spending.

Equities – Strong Fundamentals, Full Valuations

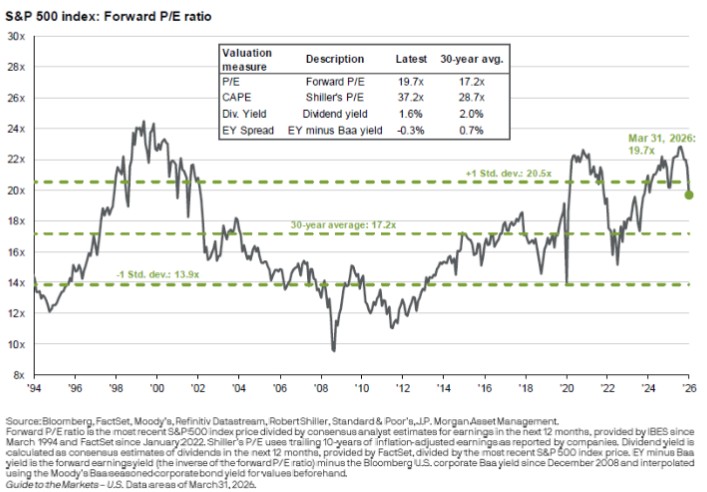

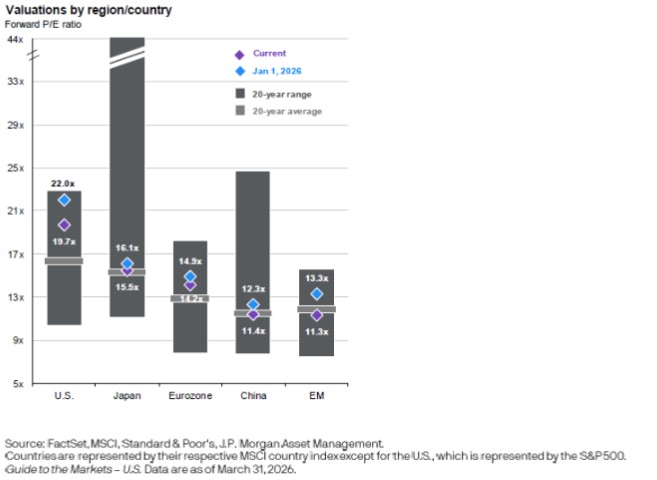

U.S. equities continue to be supported by earnings growth, but valuations are no longer cheap. The S&P 500 currently trades at approximately 19.7x forward earnings, modestly above its 30-year average of 17.2x.

This places the market in a range where future returns are likely to be more muted and increasingly dependent on continued earnings delivery rather than multiple expansion.

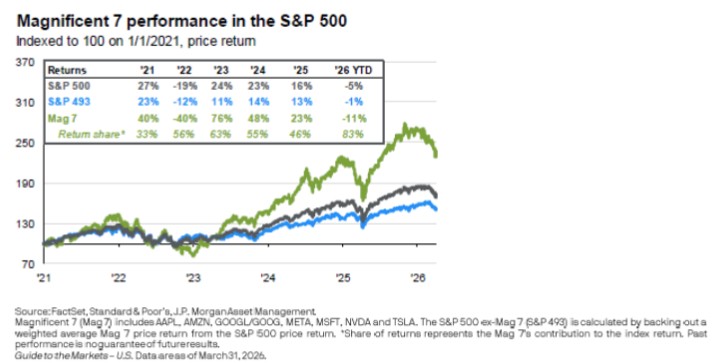

Importantly, market concentration remains elevated. The top 10 companies now represent roughly 38% of the S&P 500’s market capitalization. While these companies have delivered strong earnings and performance, this level of concentration introduces both opportunity and risk. A narrow leadership group can sustain markets, but it also increases vulnerability if leadership falters.

The influence of the “Magnificent 7” remains significant, accounting for a large share of returns in recent years, though 2026 has shown some early signs of performance dispersion.

This may indicate a gradual broadening of market participation—something that would be constructive if sustained.

This may indicate a gradual broadening of market participation—something that would be constructive if sustained.

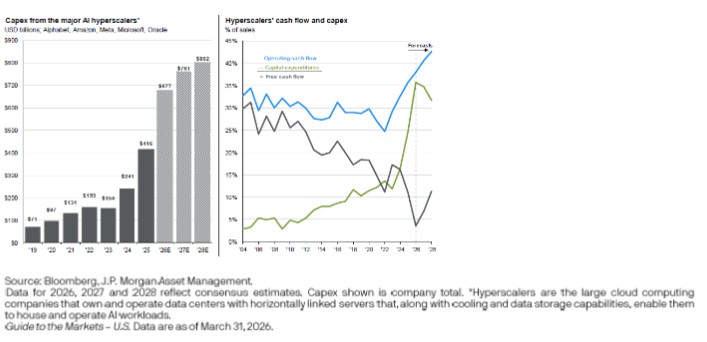

At the same time, the AI investment cycle continues to accelerate. Capital expenditures from major hyperscalers are projected to rise dramatically—from under $100 billion in 2020 to over $800 billion by 2028. While this supports earnings growth in the near term, it also raises a key open question: when and how these investments translate into durable returns.

Inflation – Normalizing, but Energy Prices complicate the picture

Inflation – Normalizing, but Energy Prices complicate the picture

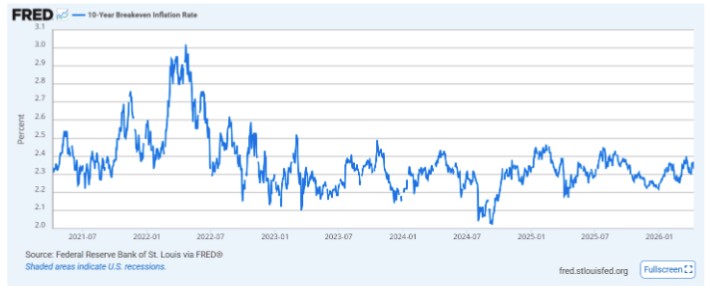

Inflation has continued to normalize, with headline CPI declining to approximately 2.4% year-over-year as of early 2026, a significant improvement from the 9% peak in 2022 (page 22). However, progress has become more incremental, particularly in services-related components. The war in Iran has caused spot oil prices to rise dramatically, but interestingly, the bond market has shown muted concern, with 10-year Breakeven Inflation rates still close to historical averages.

The Federal Reserve now faces a more nuanced challenge. With inflation closer to target but growth slowing, policy is likely to remain cautious. Market expectations suggest a gradual path for rates rather than an aggressive easing cycle.

The Federal Reserve now faces a more nuanced challenge. With inflation closer to target but growth slowing, policy is likely to remain cautious. Market expectations suggest a gradual path for rates rather than an aggressive easing cycle.

Fixed Income – Income Returns to the Forefront

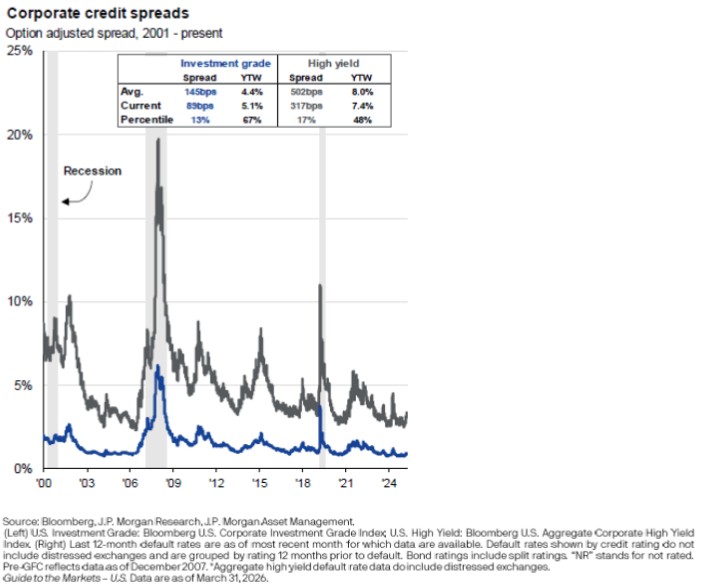

One of the more notable shifts in the current environment is the re-emergence of income in fixed-income markets. The U.S. Aggregate Bond Index now yields approximately 4.6%, which historically has been a strong predictor of forward returns—implying roughly mid-single-digit annualized returns over the next five years. Credit markets remain relatively well-behaved. Spreads are below long-term averages, and default rates, particularly in high yield, remain contained. This suggests that, for now, markets are not pricing in a significant deterioration in economic conditions.

Global Markets – Divergence Persists

Global Markets – Divergence Persists

Outside the U.S., performance remains mixed. While some emerging markets have shown resilience, developed international markets continue to lag, and structural challenges—particularly in China—persist.

Valuations outside the U.S. remain more attractive on a relative basis, but this discount has been persistent for years and reflects differences in growth, profitability, and sector composition.

Currency dynamics also remain an important driver. The U.S. dollar has been relatively stable, supported in part by interest rate differentials, though this remains a variable to watch.

Currency dynamics also remain an important driver. The U.S. dollar has been relatively stable, supported in part by interest rate differentials, though this remains a variable to watch.

Private Markets and Structural Trends

Two structural trends are worth highlighting.

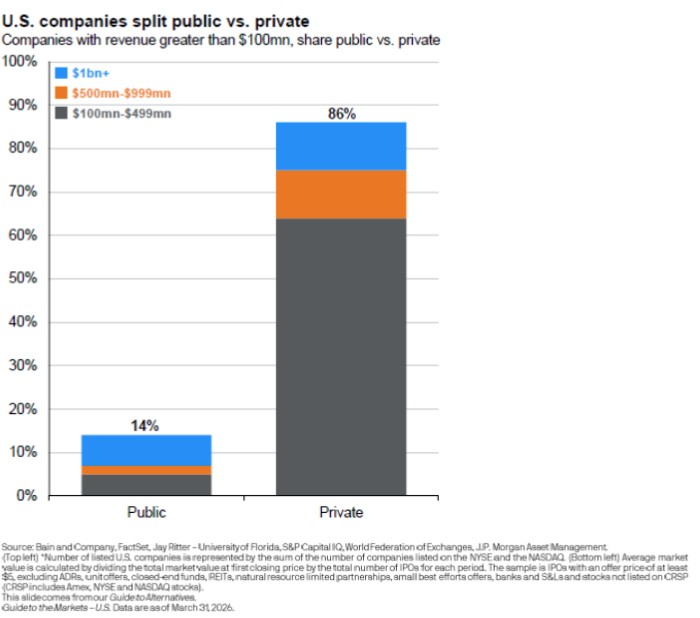

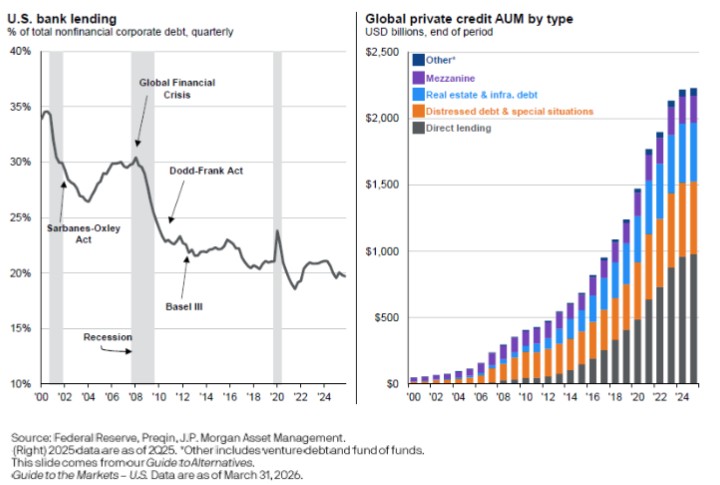

First, the continued growth of private markets. The number of publicly listed companies has declined meaningfully over time, while private capital—particularly private credit—has expanded significantly. This shift has implications for liquidity, transparency, and risk dispersion across the financial system.

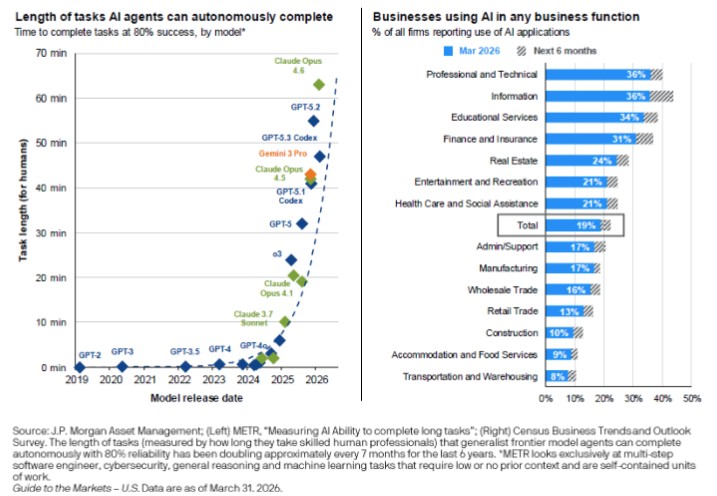

Second, the increasing role of AI—not just as a market theme, but as a broader economic driver. Adoption rates across industries continue to rise, and capabilities are advancing rapidly. While the long-term impact is likely significant, the near-term investment implications remain uncertain.

In summary, the markets present the following picture:

- Solid economic fundamentals

- Strong corporate earnings

- Elevated but not extreme valuations

- Persistent geopolitical and macro uncertainty

The consensus view is that the economy is moving toward a soft landing. We would assign a moderate probability—approximately 60–70%—to this outcome. However, there remains a meaningful risk (20–30%) that the lagged effects of higher interest rates lead to a more pronounced slowdown. A smaller probability (10–15%) exists that inflation proves more persistent than expected, keeping short rates elevated and leading to a deeper economic slowdown.

From a portfolio perspective, this is an environment where discipline matters more than prediction.

Markets may continue to appear chaotic on the surface, but as with the inverted swan analogy, the underlying drivers remain more stable than headlines suggest. Earnings, income, and diversification—not short-term narratives—continue to be the primary determinants of long-term outcomes.

As always, we appreciate your continued trust and partnership. Please do not hesitate to reach out with any questions.

Sources: J.P. Morgan Guide to the Markets (as of March 31, 2026), Federal Reserve Bank of St Louis via FRED, Bureau of Labor Statistics vis FRED,