Advice from a Wealth Manager Who Has Experienced It Firsthand

As a wealth manager, my job is to help protect my clients’ wealth — not just from market risk or taxes, but from the very real and growing threat of identity theft. Unfortunately, this is not just professional advice I’m sharing — it’s personal. I’ve lived through identity theft myself, and I can tell you, it’s not just an inconvenience. It’s a violation that affects your finances, your sense of security, and even your peace of mind.

If you ever find yourself in this position — whether it’s fraudulent unemployment claims, unauthorized credit cards, or someone impersonating you — here are the critical steps you need to take immediately.

Step 1: File a Police Report

Your first call should be to your local police department’s non-emergency line to file a police report. This creates an official record of the crime — something creditors, financial institutions, and even credit bureaus may request as you work to clear your name.

Be sure to keep the case number they provide you. You’ll need this for the next steps, especially when placing fraud alerts with credit agencies.

Step 2: Notify Your Financial Institutions

Next, alert every financial institution you work with — banks, credit card companies, investment custodians, and even lenders. Let them know you are a victim of identity theft and ask them to flag your accounts for suspicious activity.

In some cases, you may want to request new account numbers or additional security measures like verbal passcodes when calling in.

Step 3: Report Unemployment Fraud (If Applicable)

If someone has fraudulently filed for unemployment benefits in your name — a common scheme I’ve seen — you’ll need to report this directly to your state’s Employment Security Department. Each state has its own process, and acting quickly helps prevent the payment from being issued in your name.

For quick reference:

- Washington State: https://esd.wa.gov/unemployment/unemployment-benefits-fraud | 800-246-9763 | esdfraud@esd.wa.gov

- Oregon: https://www.oregon.gov/employ/Unemployment/Pages/Fraud.aspx | 877-668-3204 | Fraud Referral Form

Step 4: Review Your Credit Reports

This is critical. You need to review all three of your credit reports — from Experian, Equifax, and TransUnion — to check for any accounts, loans, or inquiries you don’t recognize.

The good news: you can get your credit reports for free at www.annualcreditreport.com. I recommend making this review part of your regular financial routine, even if you’re not a victim.

Step 5: Place Fraud Alerts on Your Credit File

Contact each of the three major credit bureaus and request a fraud alert on your file. This tells creditors to take extra steps before issuing credit in your name. It’s free and lasts for one year, with the option to extend if needed.

Here’s where to place fraud alerts:

- Experian: https://www.experian.com/fraud/center.html

- TransUnion: https://www.transunion.com/fraud-alerts

- Equifax: https://www.equifax.com/personal/credit-report-services/credit-fraud-alerts/

Step 6: Freeze Your Credit (Optional but Highly Recommended)

If you want an even stronger layer of protection, you can freeze your credit with all three bureaus. A credit freeze completely locks down your credit file, making it impossible for anyone — including you — to open new accounts until you temporarily “thaw” the freeze.

It’s free to place and lift a freeze, and most credit bureaus offer easy-to-use tools to manage the process. Just be sure to keep your passwords in a safe place — you’ll need them if you apply for a mortgage, car loan, or any other type of credit in the future.

Step 7: Report the Theft to the Federal Trade Commission (FTC)

Finally, file a report with the Federal Trade Commission at www.identitytheft.gov. This creates an official record at the national level, and the site offers a wealth of resources to help you recover your identity.

Your FTC Identity Theft Report can also be used to help dispute fraudulent accounts with creditors and credit bureaus.

Final Thoughts — From Someone Who’s Been There

I know firsthand how overwhelming this process feels. When I discovered my own identity had been stolen, I felt a mixture of anger, confusion, and vulnerability that’s hard to describe. I also know that acting swiftly and decisively made all the difference in minimizing the damage.

As your wealth manager — and as someone who’s walked this road — my advice is this:

- Be proactive. Review your credit regularly and set up monitoring alerts so you can catch issues early.

- Be organized. Document every step you take — every call, email, and case number.

- Be patient. Recovery is a process, not a single phone call.

- And don’t be afraid to ask for help. Whether it’s your advisor, an attorney, or a trusted identity theft resolution service, having a professional advocate in your corner can make a world of difference.

If you’ve been impacted — or if you just want to know how to protect yourself before it happens — please reach out. This is part of what I do for clients every day, and I’m always happy to help.

Your wealth is important — and so is your identity. Let’s protect both.

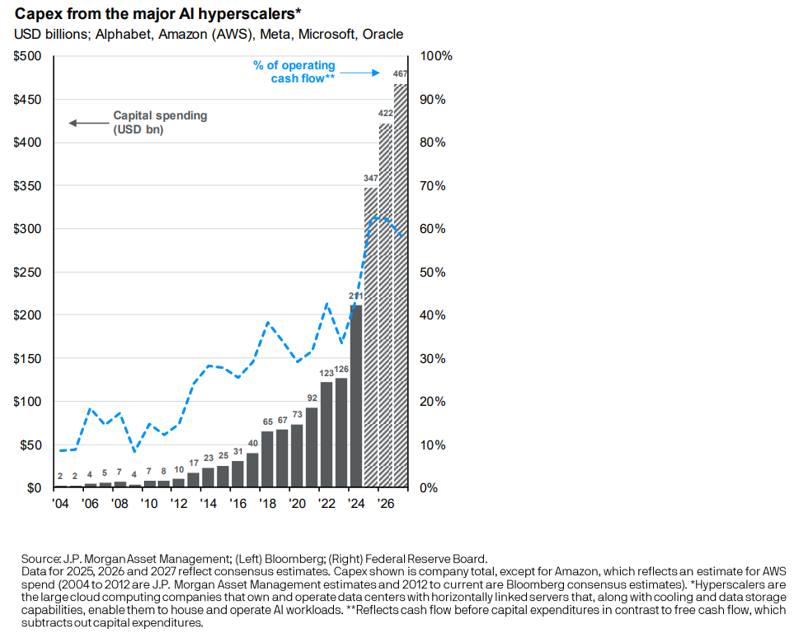

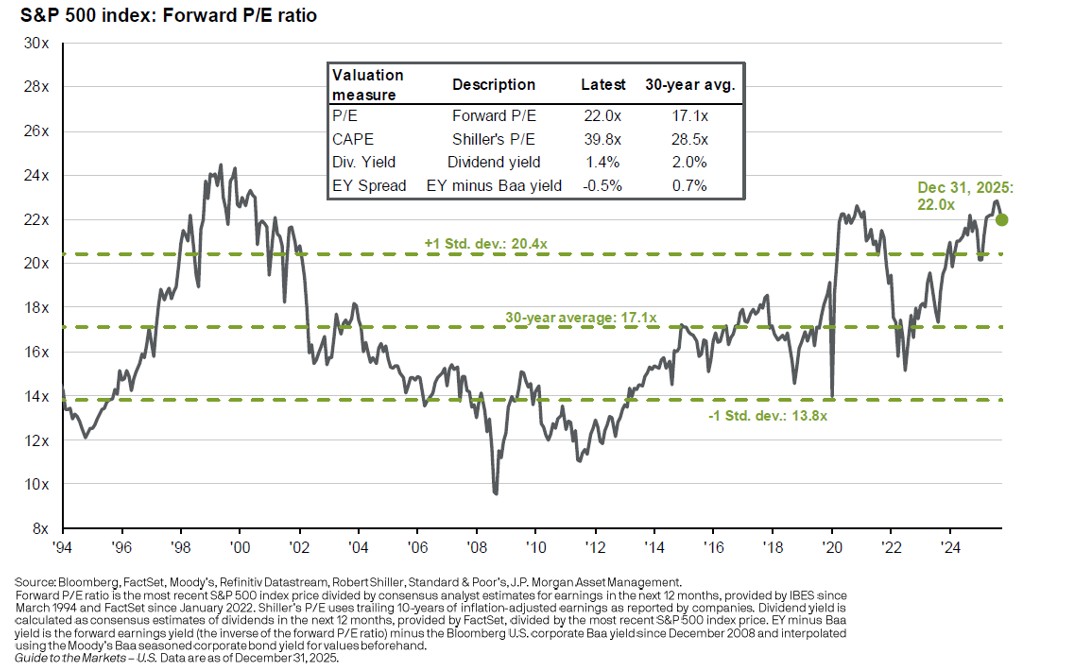

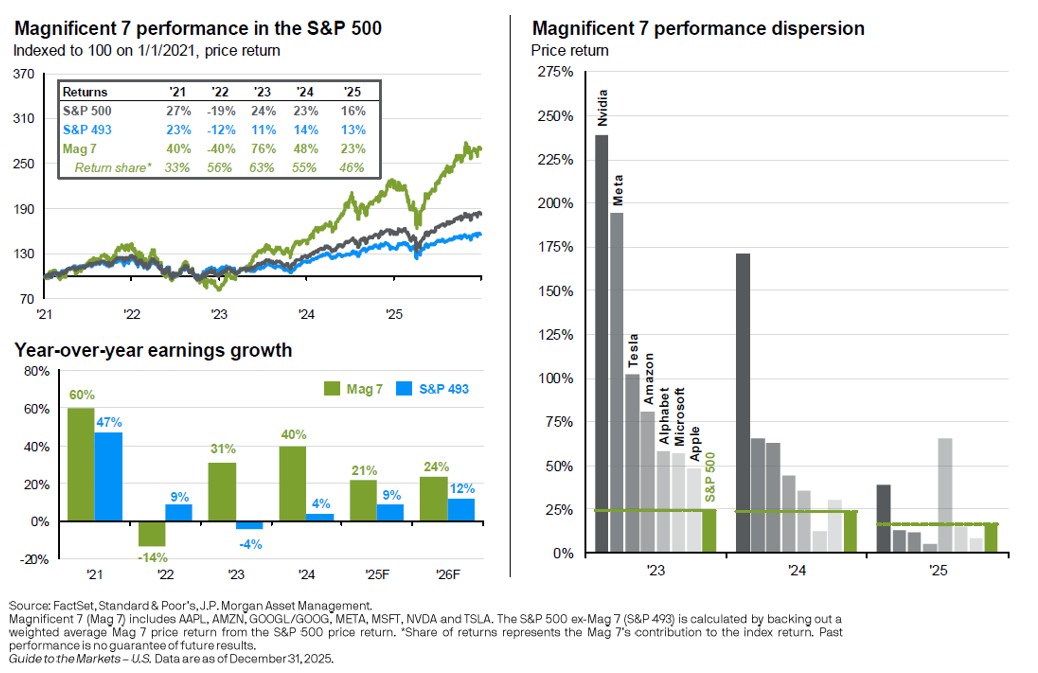

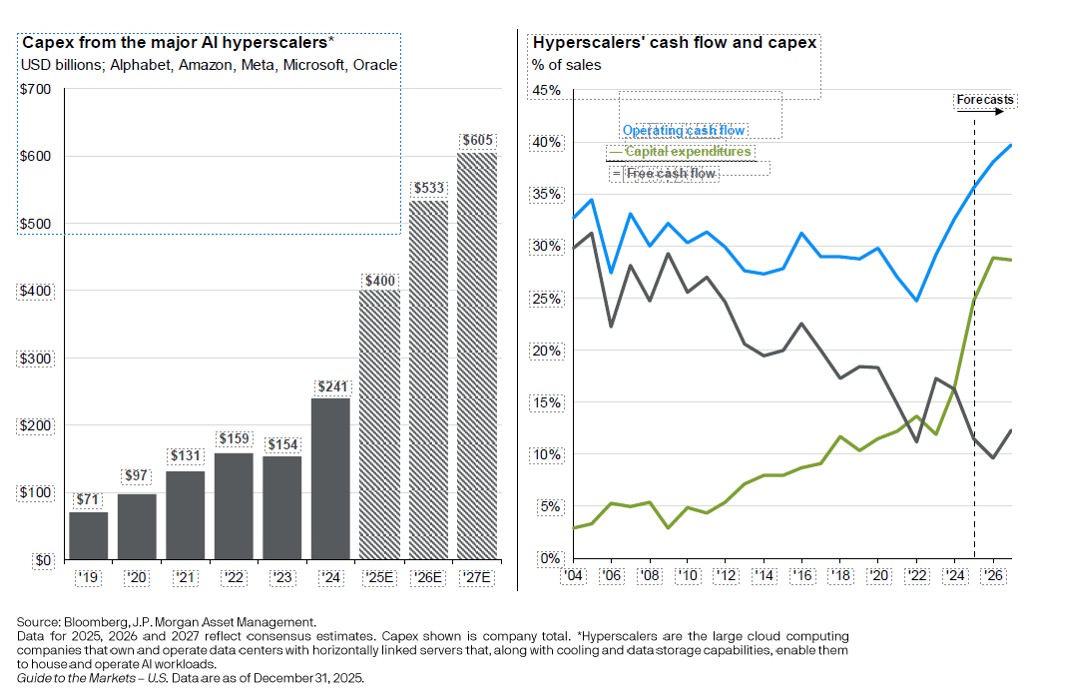

Much of this dominance has been reinforced by the extraordinary surge in capital spending related to artificial intelligence. The largest U.S. technology companies are at the center of a massive investment cycle, committing hundreds of billions of dollars toward data centers, semiconductors, cloud infrastructure, and AI model development. Planned capital expenditures by the major AI hyperscalers have grown at a staggering pace and are expected to continue rising over the coming years.

Much of this dominance has been reinforced by the extraordinary surge in capital spending related to artificial intelligence. The largest U.S. technology companies are at the center of a massive investment cycle, committing hundreds of billions of dollars toward data centers, semiconductors, cloud infrastructure, and AI model development. Planned capital expenditures by the major AI hyperscalers have grown at a staggering pace and are expected to continue rising over the coming years.

As with past technology cycles, the long-term winners are likely to be those companies that can translate scale and innovation into durable cash flows, rather than simply the largest spenders.

As with past technology cycles, the long-term winners are likely to be those companies that can translate scale and innovation into durable cash flows, rather than simply the largest spenders. International Equities: A Long-Awaited Broadening

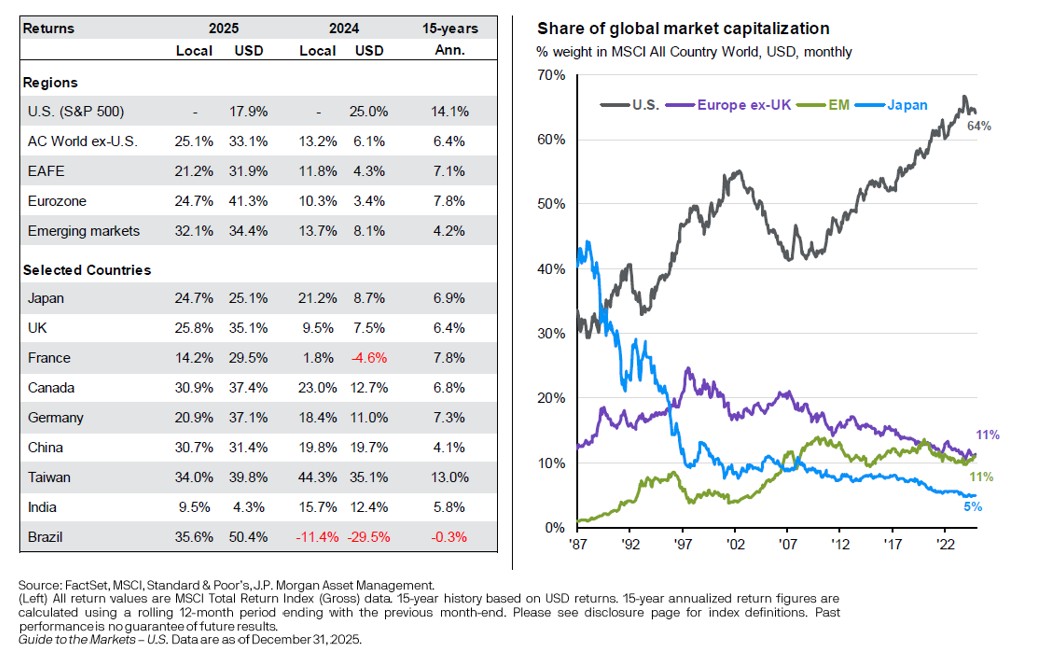

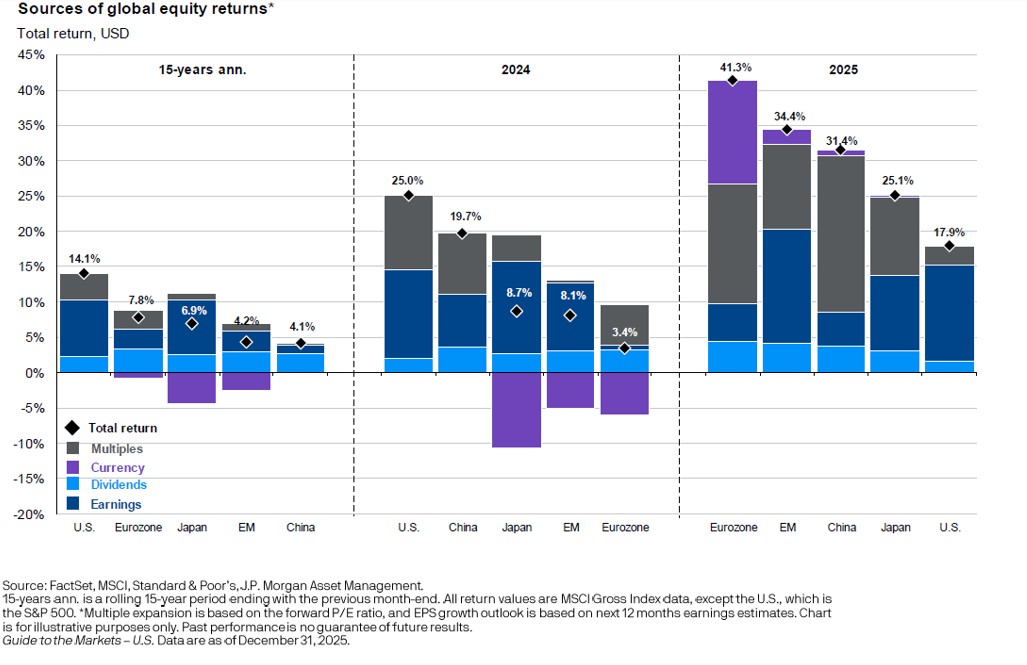

International Equities: A Long-Awaited Broadening This was notable because international equities outperformed the U.S. during a year when U.S. stocks themselves delivered strong, above-trend returns. Rather than a rotation away from U.S. assets, 2025 reflected a broadening of opportunity.

This was notable because international equities outperformed the U.S. during a year when U.S. stocks themselves delivered strong, above-trend returns. Rather than a rotation away from U.S. assets, 2025 reflected a broadening of opportunity. Performance varied by region. Japan benefited from improved corporate governance and earnings momentum; Europe saw strong gains in the banking sector as growth stabilized; and emerging markets experienced strength in countries such as China, India and Taiwan. A weaker U.S. dollar further supported international returns, consistent with historical periods of non-U.S. outperformance.

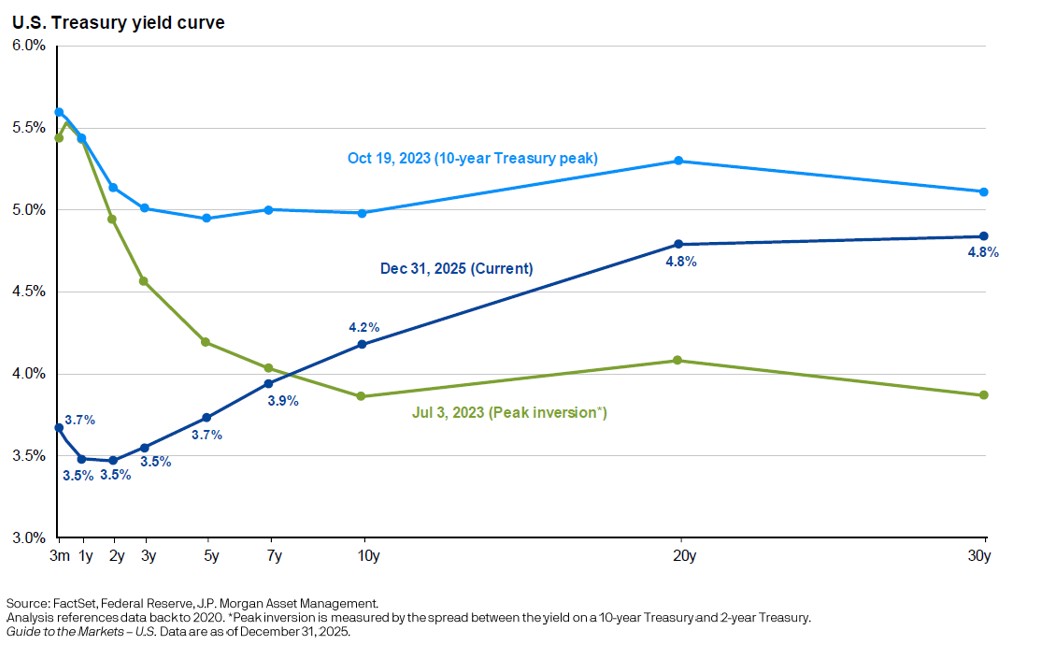

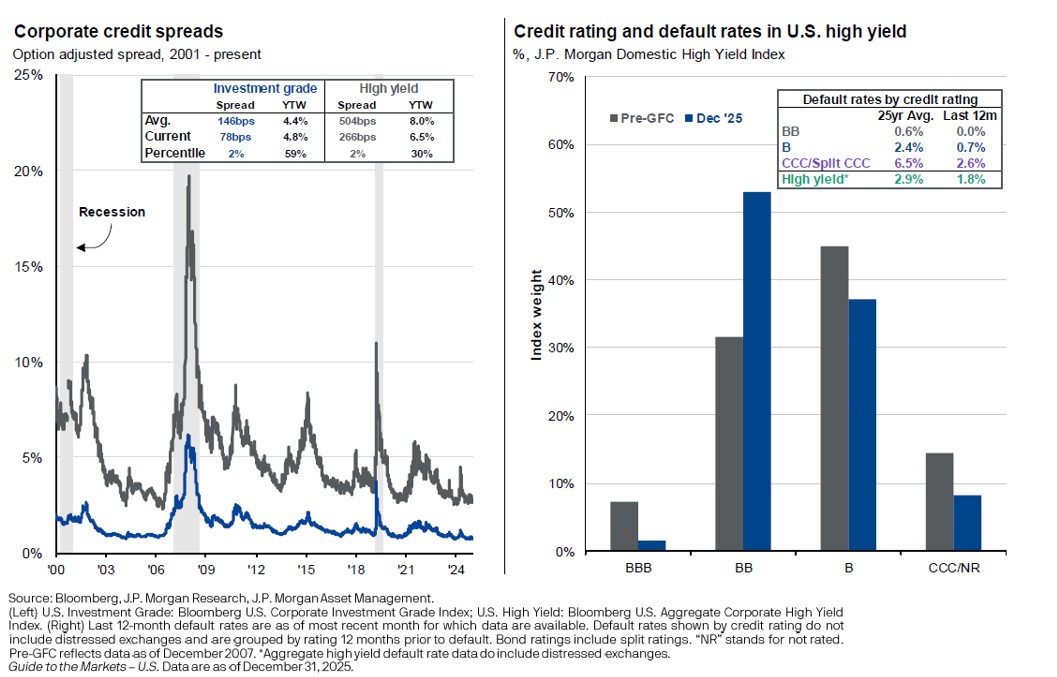

Performance varied by region. Japan benefited from improved corporate governance and earnings momentum; Europe saw strong gains in the banking sector as growth stabilized; and emerging markets experienced strength in countries such as China, India and Taiwan. A weaker U.S. dollar further supported international returns, consistent with historical periods of non-U.S. outperformance. The Federal Reserve signaled that policy rates are likely to trend gradually lower over time, toward a long-run level near 3.0%, assuming continued progress on inflation. Credit markets remained healthy, with investment-grade and high-yield spreads near the lower end of historical ranges and default rates well contained.

The Federal Reserve signaled that policy rates are likely to trend gradually lower over time, toward a long-run level near 3.0%, assuming continued progress on inflation. Credit markets remained healthy, with investment-grade and high-yield spreads near the lower end of historical ranges and default rates well contained.

Looking Ahead

Looking Ahead