Markets have a way of humbling consensus views. Entering 2025, many investors expected a narrow path to returns—led once again by a small group of U.S. stocks, with little help from bonds or international markets. Instead, the year delivered something different: strong absolute returns, broader participation across regions, and a re-emergence of diversification as a meaningful contributor to results. It was a reminder that market leadership does not move in straight lines—and that patient, diversified investors are often rewarded when expectations are most one-sided.

U.S. Equities: Strong Results, Higher Expectations

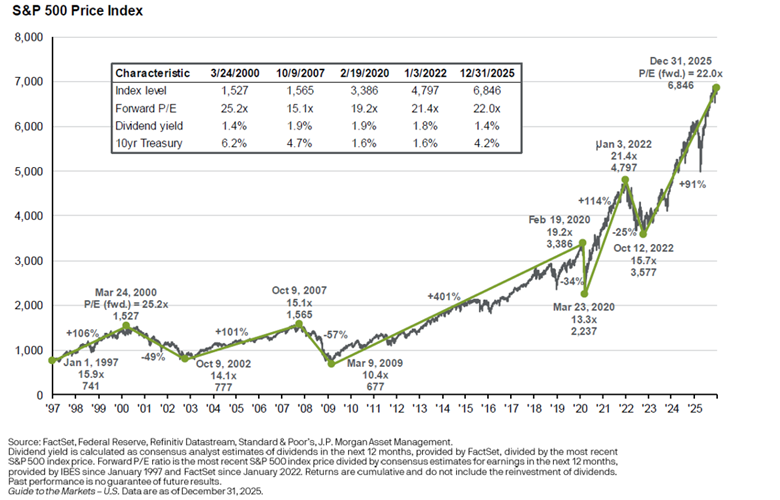

U.S. stocks delivered another solid year. The S&P 500 finished 2025 at 6,846, generating a 17.9% total return per Bloomberg. Economic growth remained resilient, inflation continued to cool, and corporate earnings proved more durable than many had anticipated.

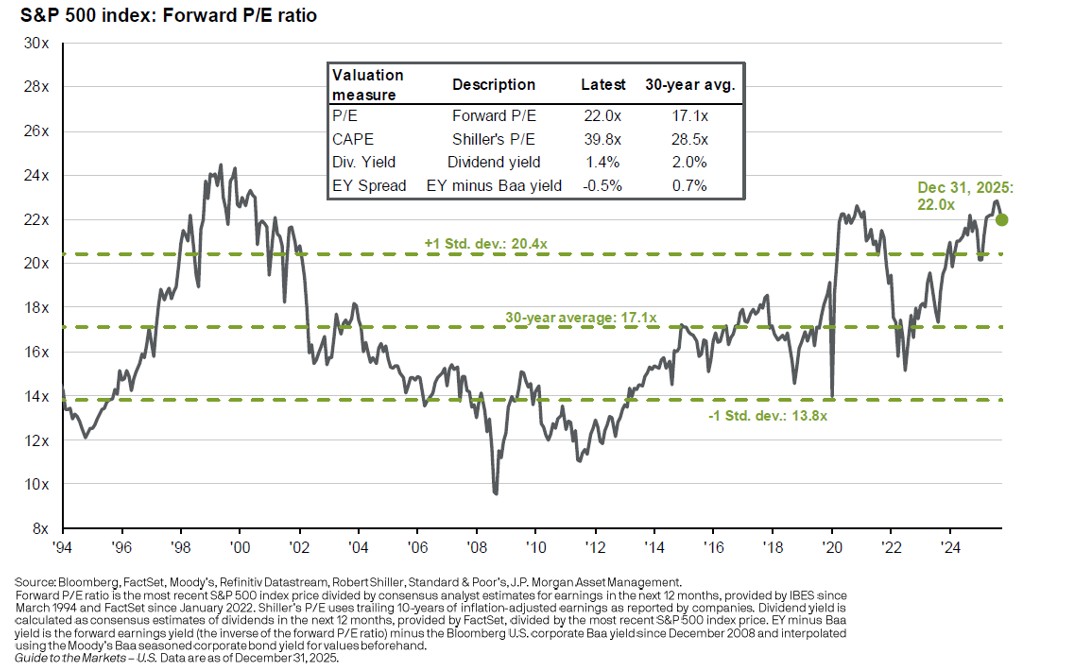

At the same time, optimism became increasingly reflected in prices. The S&P 500 ended the year trading at a forward price-to-earnings ratio of 22.0x, well above its 30-year average of 17.1x.

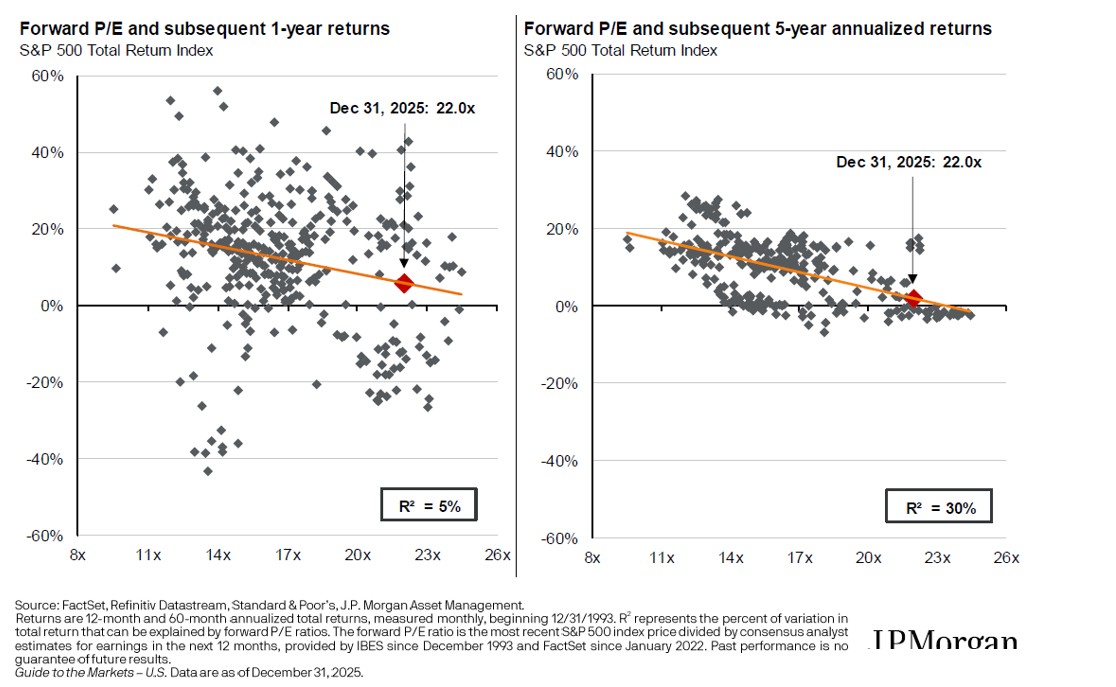

Valuations are not a reliable guide to short-term market movements, but they do matter over longer horizons. Historically, starting valuations have shown a much stronger relationship with five-year forward returns than with one-year results.

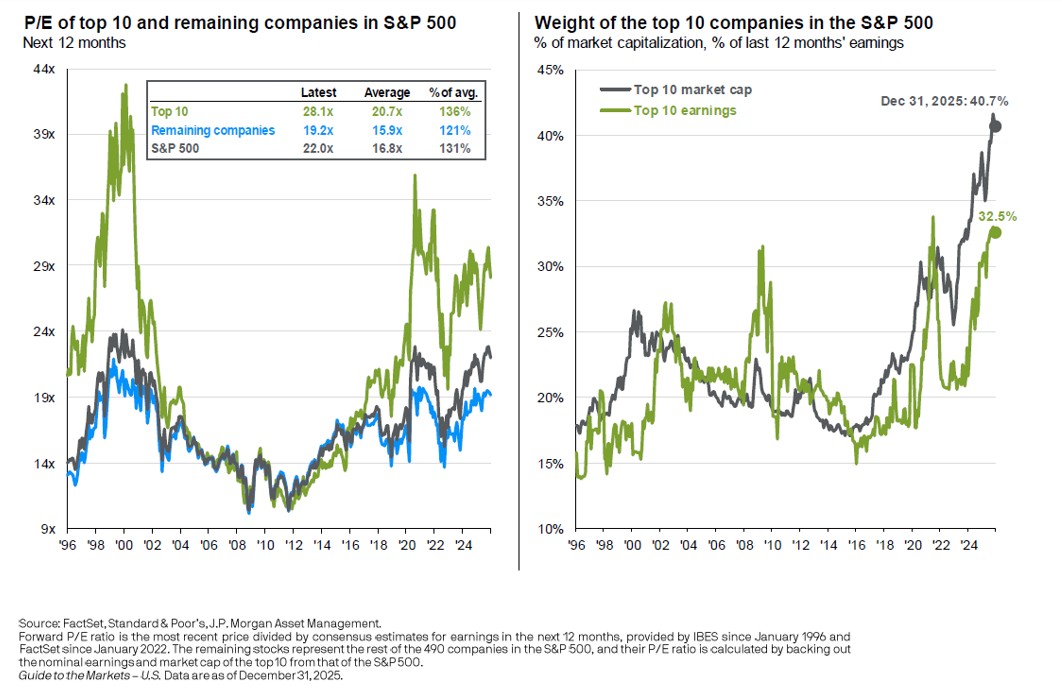

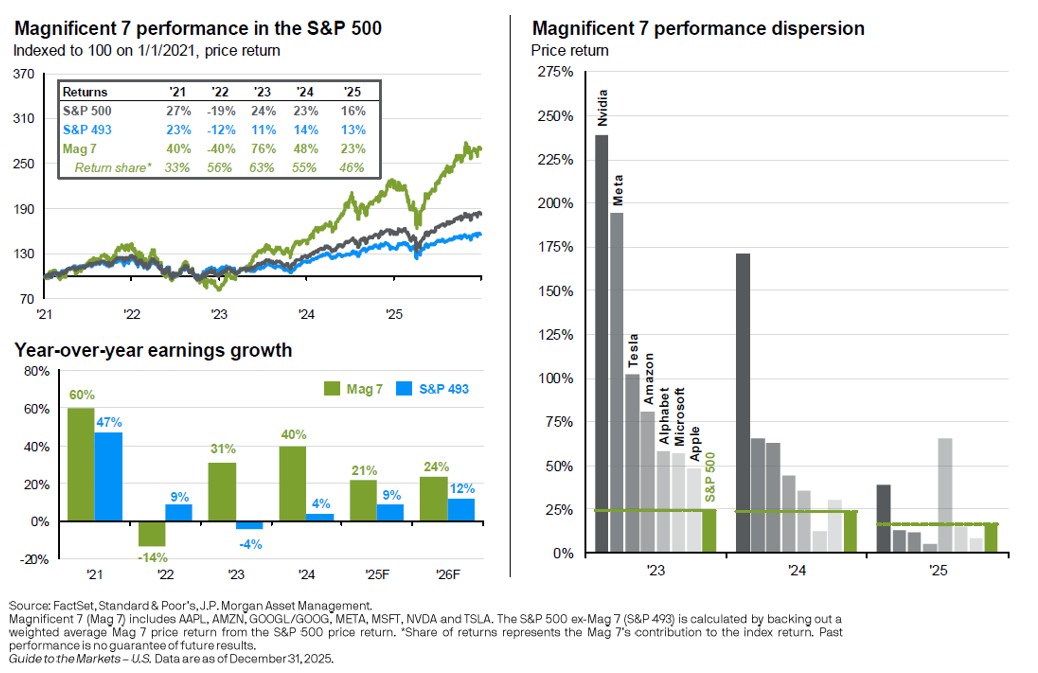

Market concentration remained elevated. The ten largest companies now represent roughly 40.7% of the S&P 500, near historical extremes.

The “Magnificent 7” again accounted for a disproportionate share of returns—about 46% of index performance in 2025—reflecting their scale, profitability, and earnings momentum.

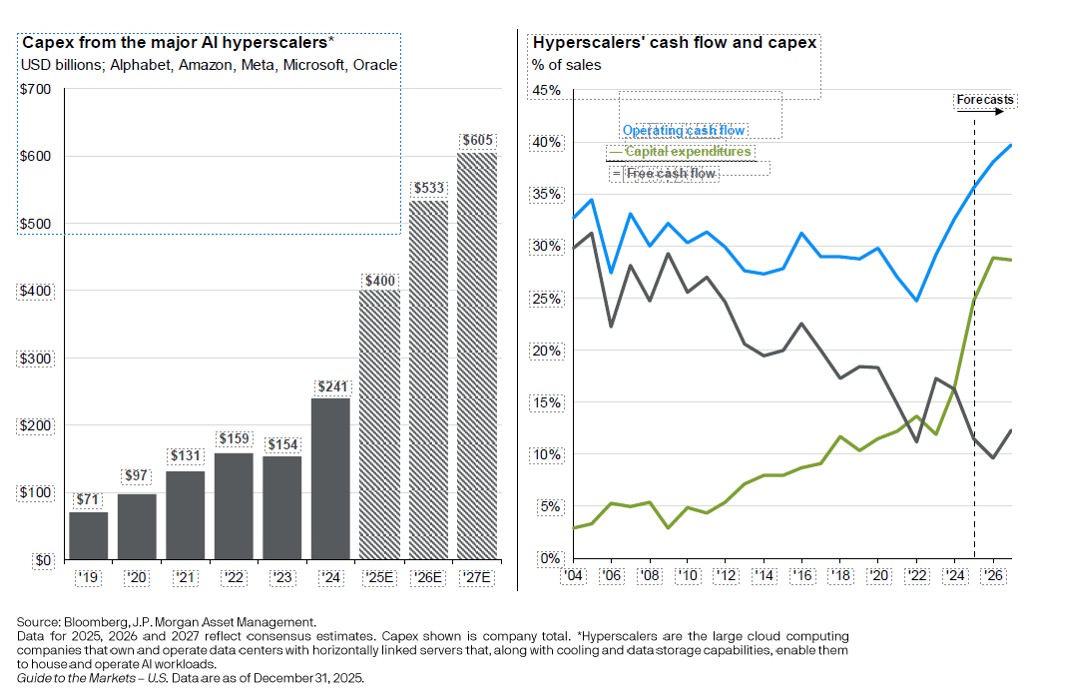

Much of this dominance has been reinforced by the extraordinary surge in capital spending related to artificial intelligence. The largest U.S. technology companies are at the center of a massive investment cycle, committing hundreds of billions of dollars toward data centers, semiconductors, cloud infrastructure, and AI model development. Planned capital expenditures by the major AI hyperscalers have grown at a staggering pace and are expected to continue rising over the coming years.

Much of this dominance has been reinforced by the extraordinary surge in capital spending related to artificial intelligence. The largest U.S. technology companies are at the center of a massive investment cycle, committing hundreds of billions of dollars toward data centers, semiconductors, cloud infrastructure, and AI model development. Planned capital expenditures by the major AI hyperscalers have grown at a staggering pace and are expected to continue rising over the coming years.

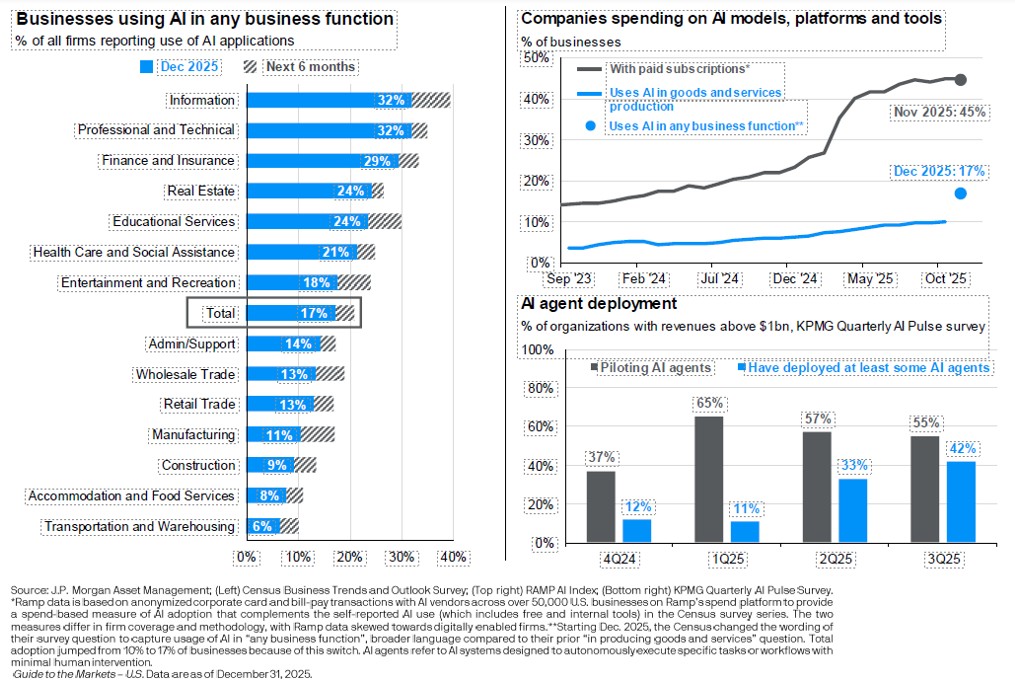

This level of investment has naturally fueled investor enthusiasm around AI’s long-term potential, but it also raises reasonable questions about returns on invested capital. In 2025, investors periodically expressed concern around whether some companies—such as Oracle and Meta—would ultimately earn attractive returns on this spending, leading to periods of volatility. Even so, the data make clear that capital markets remain willing to fund this investment cycle, with AI adoption broadening across industries and corporate spending on AI tools continuing to accelerate.

As with past technology cycles, the long-term winners are likely to be those companies that can translate scale and innovation into durable cash flows, rather than simply the largest spenders.

As with past technology cycles, the long-term winners are likely to be those companies that can translate scale and innovation into durable cash flows, rather than simply the largest spenders.

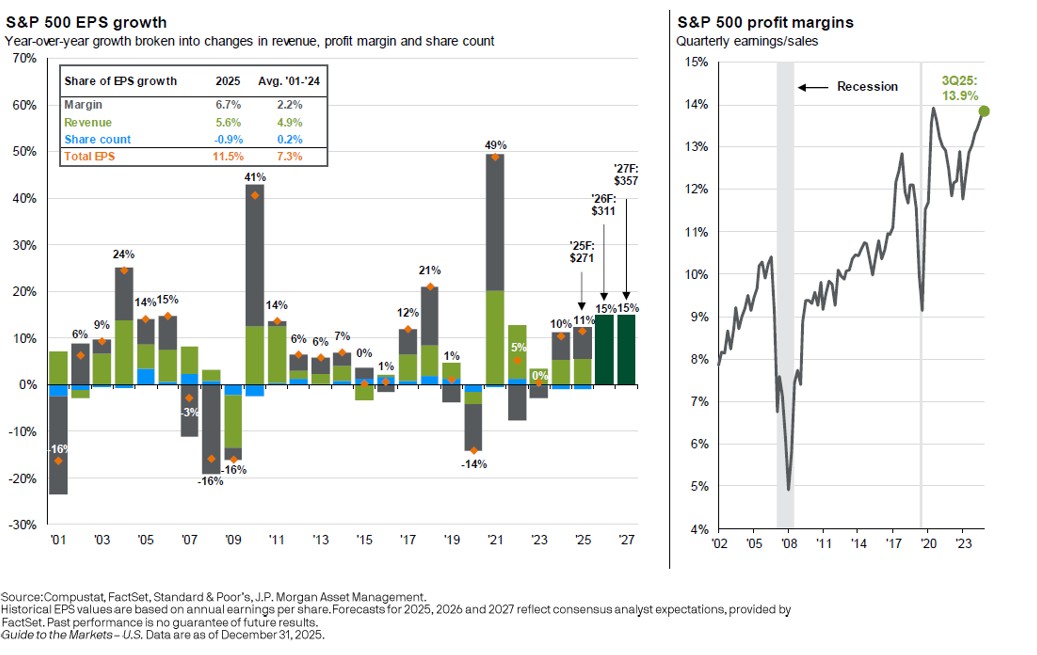

Corporate fundamentals, however, remain supportive. Profit margins reached approximately 13.9% in the third quarter, well above long-term averages, and earnings expectations for 2026 remain constructive. Still, margins at these levels leave less room for error should growth slow or costs rise.

International Equities: A Long-Awaited Broadening

International Equities: A Long-Awaited Broadening

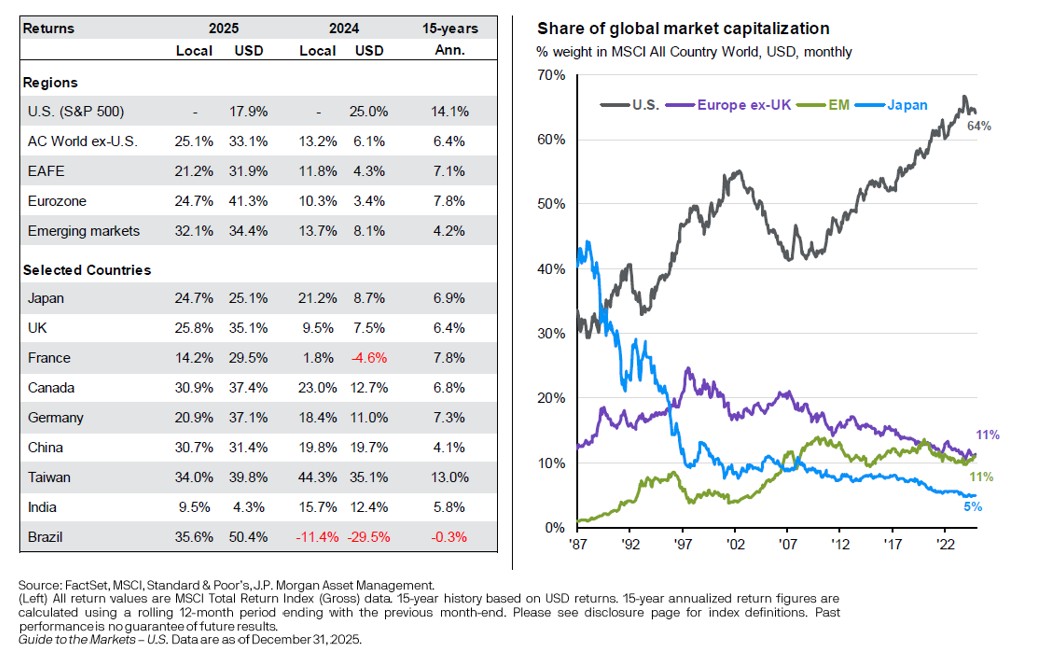

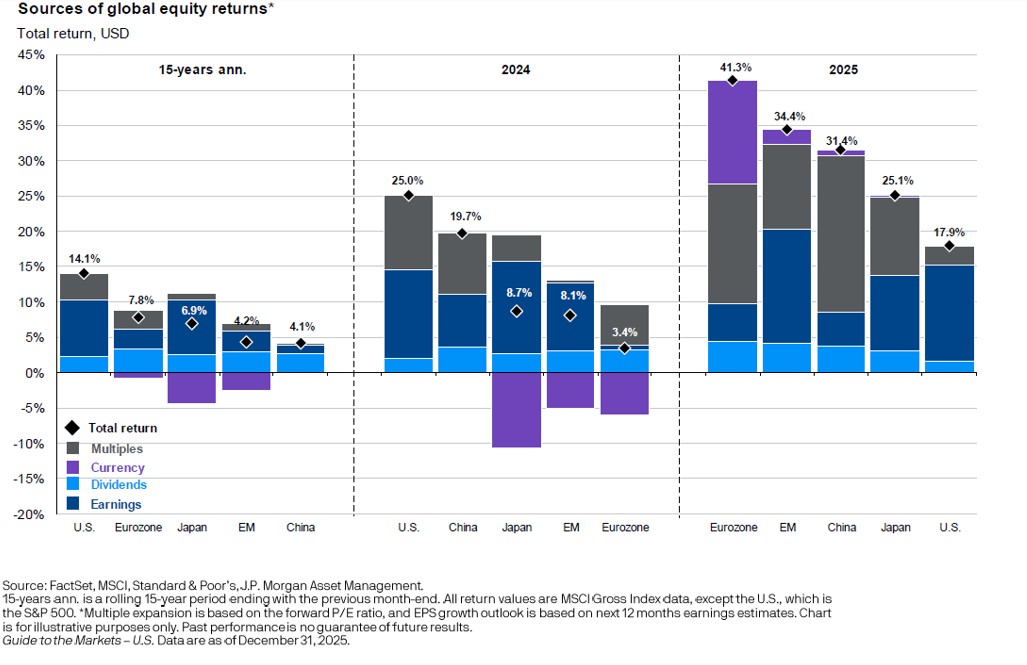

One of the most important developments of 2025 was the return of international equity leadership. Markets outside the U.S. did not simply perform well—they meaningfully outperformed U.S. equities despite strong U.S. returns. The MSCI All Country World ex-U.S. Index gained 32.39% in 2025 per MSCI, far exceeding the S&P 500’s advance.

This was notable because international equities outperformed the U.S. during a year when U.S. stocks themselves delivered strong, above-trend returns. Rather than a rotation away from U.S. assets, 2025 reflected a broadening of opportunity.

This was notable because international equities outperformed the U.S. during a year when U.S. stocks themselves delivered strong, above-trend returns. Rather than a rotation away from U.S. assets, 2025 reflected a broadening of opportunity.

Valuations played an important role. International equities entered the year trading at a 30–40% discount to U.S. markets, a gap that remains wide by historical standards. Over the past decade, U.S. equity returns have benefited significantly from rising valuation multiples, while international returns have relied more on earnings growth, dividends, and currency movements. In 2025, those factors aligned more favorably outside the U.S.

Performance varied by region. Japan benefited from improved corporate governance and earnings momentum; Europe saw strong gains in the banking sector as growth stabilized; and emerging markets experienced strength in countries such as China, India and Taiwan. A weaker U.S. dollar further supported international returns, consistent with historical periods of non-U.S. outperformance.

Performance varied by region. Japan benefited from improved corporate governance and earnings momentum; Europe saw strong gains in the banking sector as growth stabilized; and emerging markets experienced strength in countries such as China, India and Taiwan. A weaker U.S. dollar further supported international returns, consistent with historical periods of non-U.S. outperformance.

For long-term investors, 2025 served as a reminder that international markets can play a meaningful role—not only as diversifiers, but as contributors to returns.

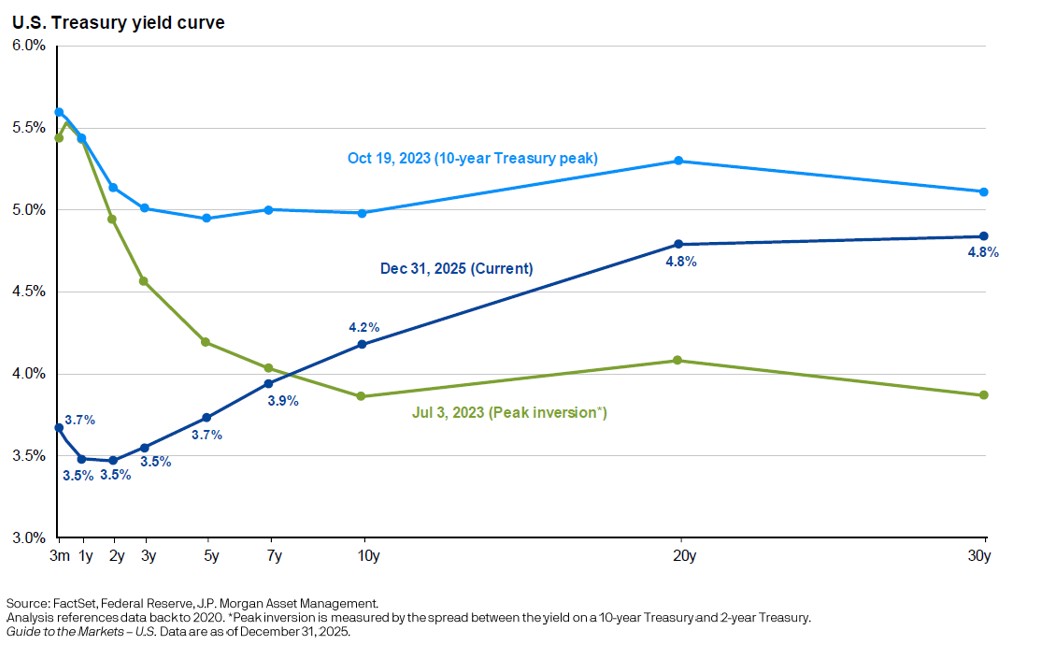

Fixed Income: A More Familiar Role Returns

After several challenging years, fixed income regained its footing. The 10-year U.S. Treasury yield ended the year near 4.2%, and the yield curve moved back into modestly positive territory following a prolonged inversion.

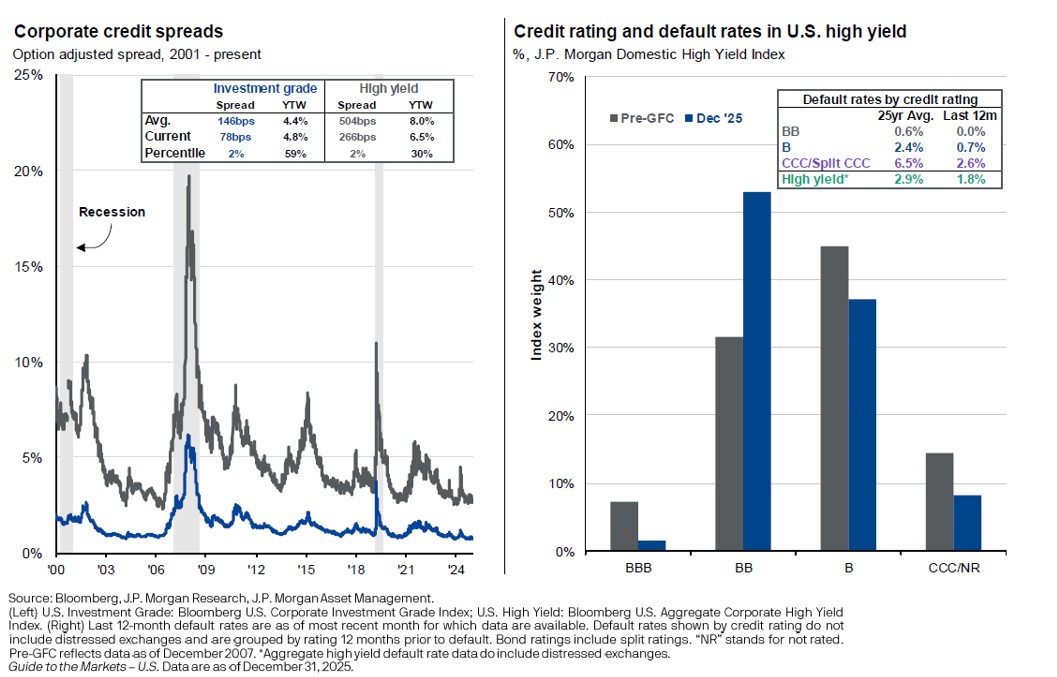

The Federal Reserve signaled that policy rates are likely to trend gradually lower over time, toward a long-run level near 3.0%, assuming continued progress on inflation. Credit markets remained healthy, with investment-grade and high-yield spreads near the lower end of historical ranges and default rates well contained.

The Federal Reserve signaled that policy rates are likely to trend gradually lower over time, toward a long-run level near 3.0%, assuming continued progress on inflation. Credit markets remained healthy, with investment-grade and high-yield spreads near the lower end of historical ranges and default rates well contained.

Just as importantly, starting yields matter once again. With the Bloomberg U.S. Aggregate yield near 4.3%, history suggests five-year annualized returns in the 4–5% range, a meaningful improvement compared with much of the past decade.

Looking Ahead

Looking Ahead

The experience of 2025 reinforces several principles that continue to guide our approach:

- Strong markets can coexist with rising valuation risk

- Market leadership can remain concentrated longer than expected—but eventually broadens

- Diversification often proves most valuable after periods when it has been least rewarded

- Fixed income once again plays a meaningful role in balanced portfolios

As we look ahead, we remain focused on building portfolios that balance participation in growth with discipline around valuation, quality, and risk management. While short-term market outcomes are inherently unpredictable, history continues to favor patient investors who stay diversified, remain disciplined, and avoid reacting to headlines.

We are grateful for the trust you place in us and look forward to navigating the opportunities and challenges ahead together.