When an athlete is performing at their highest level, it is often said that they are “in the zone” or “in the flow.” This state of complete focus and harmony—where effort feels effortless—is a goal pursued by professionals and weekend athletes alike. Legendary figures such as Kobe Bryant, Serena Williams, Tom Brady, and Mikaela Shiffrin are renowned for consistently reaching this state. Teams, too, have experienced it—think of the 1985 Chicago Bears, the Boston Red Sox of the 2000s, or the Red Bull Formula 1 team. (With some luck, perhaps the 2025 Seattle Mariners will one day join that list.)

At the risk of tempting fate, financial markets over the past quarter have also seemed to find their rhythm. Every major sector delivered positive returns, with markets rewarding good news and, for now, brushing off less favorable headlines. While this kind of synchronized momentum is encouraging, we know from both sports and markets that staying “in the flow” is not a permanent state.

U.S. Equities – Strong Earnings and AI Momentum

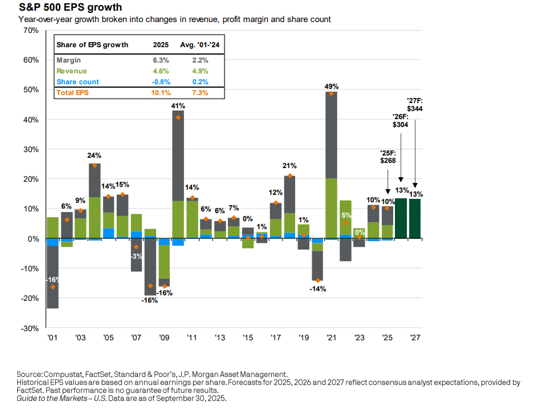

As of October 1, the S&P 500 reached a record high for the 29th time in 2025, even briefly moving above 6,700. The positive returns were underpinned by solid fundamentals: second-quarter operating earnings rose 10.55% year over year, according to Standard & Poor’s.

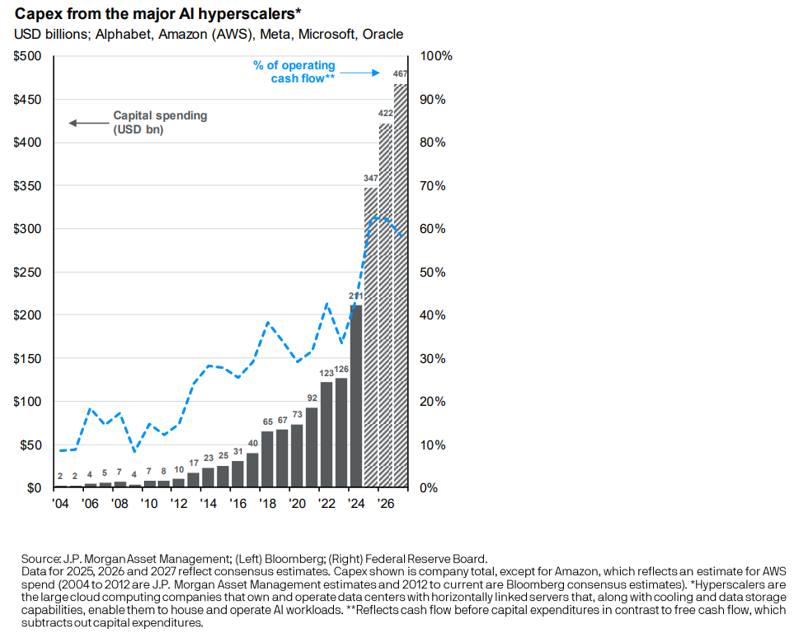

Growth companies led the way, with the Vanguard Growth ETF up 12.50% in the quarter. Value-oriented companies and small caps also advanced, though more modestly, at 6.85% and 3.50% respectively. Investors continue to reward companies tied to artificial intelligence, though the question of when those substantial investments will begin to deliver measurable returns remains open.

International Equities – Positive but Uneven

International markets also contributed to gains. Emerging markets climbed 10.11% for the quarter, and Asian developed markets advanced 7.62%. European equities trailed these regions but still managed a respectable 3.24% return.

While the breadth of international gains is encouraging, regional performance continues to diverge, underscoring the importance of diversification and careful allocation.

Fixed Income – Support from the Fed

Bonds also enjoyed a strong quarter. Signs of a softer labor market, combined with steady inflation, prompted the Federal Reserve to lower short-term interest rates by a quarter point in September. Yields moved slightly lower, and both corporate bonds and mortgage-backed securities outperformed U.S. Treasuries, helped by healthy corporate balance sheets and reduced volatility in interest rates.

Economy – Growth Signs Mixed

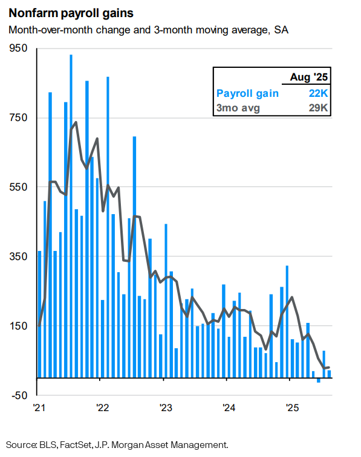

Consumers, for the most part, looked past tariff-related concerns, as many companies absorbed costs rather than passing them along. Still, revisions to labor data raised new questions: the Bureau of Labor Statistics cut its estimate of 2024 job growth by more than 900,000 positions. Forecasts for job growth in 2025 are trending below 2024 levels. Consumer spending, however, has remained resilient. High-income households, which account for over half of all consumer spending, continue to support economic activity. Whether this spending power can offset broader labor market weakness is a key trend to monitor.

Looking Ahead – Staying in Rhythm, Aware of the Clock

Corporate profits continue to expand, consumers remain willing to spend, and businesses are investing for future growth. Technology continues to dominate headlines and portfolios, with the ten largest companies in the S&P 500 now representing more than 40% of the index’s market capitalization. Such concentration highlights both the power of innovation and the importance of vigilance.

The overall backdrop remains constructive: inflation is moderating, interest rates have eased slightly, and spending is steady. Yet, just as an athlete cannot stay in the flow forever, markets eventually face disruptions. For now, the momentum is intact—but we remain mindful that the positive fundamentals that have led to this virtuous cycle will change over time.

As always, we appreciate your trust and partnership. Our focus remains on helping you navigate markets with clarity, discipline, and perspective. Please don’t hesitate to reach out with any questions.

Source: JP Morgan, Bloomberg.com, Bureau of Labor Statistics, and https://investor.vanguard.com/Vanguard