Daniel Kahneman spent much of his career studying why smart people make bad decisions, and his book ‘Thinking, Fast and Slow’ boils it down to two systems running inside every one of us. System 1 is fast, intuitive, and emotional. It reacts to a loud noise, a scary headline, a sudden price spike, before you’ve had a chance to think. System 2 is slow, deliberate, and effortful. It’s the part of your brain that actually does the math, and most people avoid engaging it whenever System 1 offers a plausible-enough answer on its own. Kahneman’s core finding was not that System 1 is bad. It is fast for a reason. His finding was that we consistently let System 1 answer questions that only System 2 is equipped to handle.

Markets run on the same two systems, and this quarter was as clean an illustration of the difference as I’ve seen in some time.

The story everyone watched

At the end of February, war broke out with Iran, and oil markets did exactly what System 1 would predict. WTI crude spiked above $112 a barrel as traders priced in the risk that the Strait of Hormuz, the channel through which roughly a fifth of the world’s oil moves, would close entirely (Bloomberg). For the better part of three months, it seemed that every headline and dinner conversation was about gas prices and the risk of a 1970s-style oil shock. That is System 1 doing its job: a threat appeared, and everyone reacted to it immediately. Then a ceasefire was announced, the strait partially reopened to traffic, and by June 30 WTI had settled back to $70 a barrel.

The crisis that dominated every conversation during April was, three months later, largely back to where it was before the crisis began.

The story almost no one watched

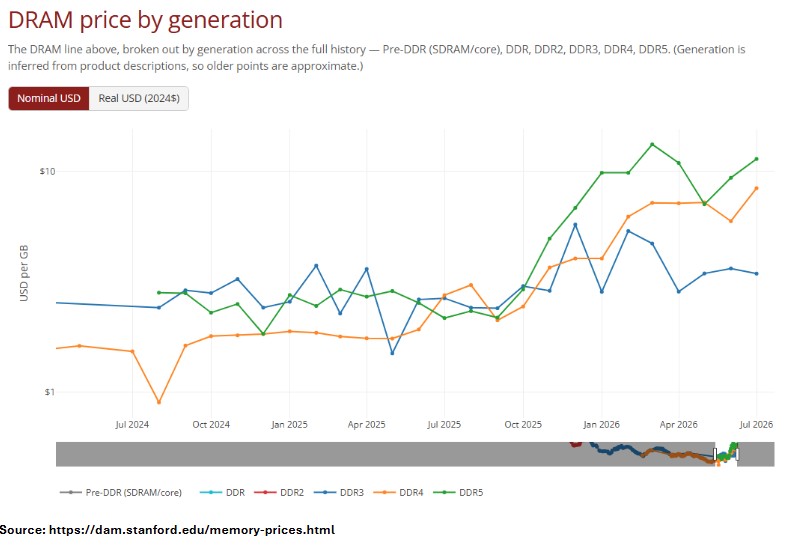

Memory chips required System 2, and that’s exactly why almost nobody engaged with the story. While oil was in the spotlight, a quieter commodity was undergoing a consequential repricing. According to Stanford University’s DRAM price index, the price of DDR4 memory rose from $2.665 per gigabyte on July 1, 2025 to $8.44 per gigabyte on July 1, 2026, an increase of more than 200% in a single year. This is not a niche input. Memory chips sit inside every smartphone, laptop, gaming console, and, most importantly, every server rack being built out for artificial intelligence. In response to the price increase, both Apple and Microsoft have announced price increase for iPhones,MacBooks and Xboxs.. Those are consumer-facing symptoms of a much larger story happening inside the data centers that the market has been paying up for.

What the data actually shows

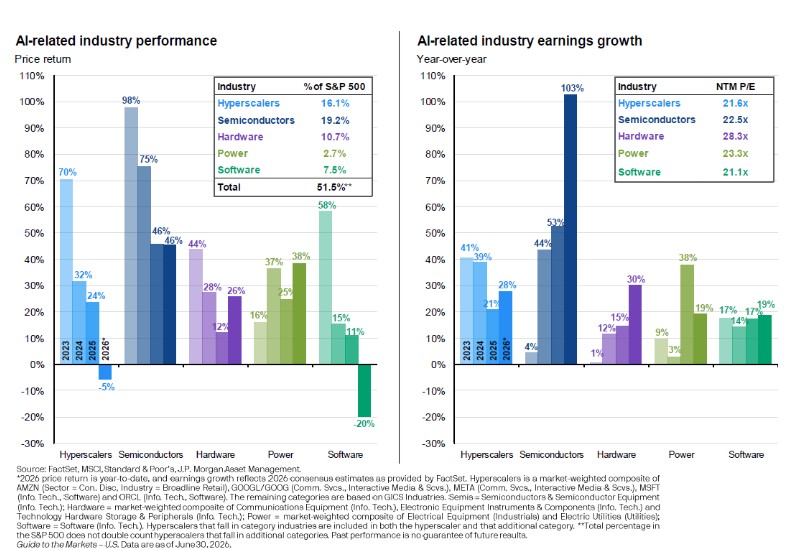

My experience as an analyst and portfolio manager have taught me that the market’s System 1 and System 2 rarely agree on price for very long. The S&P 500 gained a strong 15.2% during the second quarter, and on the surface that reads like a straightforward AI-driven tech rally. The number that actually matters is what happened underneath it. Hyperscalers, the companies whose capital spending has anchored the entire AI narrative, are down 5% year to date on a price basis. Semiconductor companies, the ones that supply them, are up 46% over the same stretch (p. 11). The market rotated from the platforms to the picks and shovels this quarter, quietly enough that most headlines are still describing this as one trade instead of two.

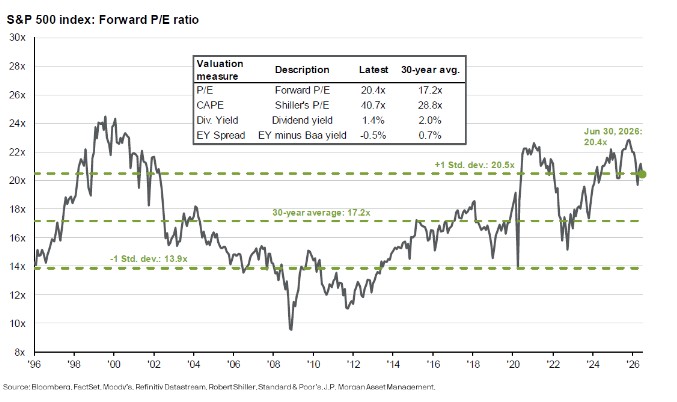

The index itself closed the quarter at 7,499, trading at a forward P/E of 20.4x versus a 30-year average of 17.2x (p. 4-5). The Shiller P/E, which smooths for a full economic cycle, sits at 40.7x against a 28.8x long-run average. Markets are not cheap, and the reason they are not cheap has a name: concentration.

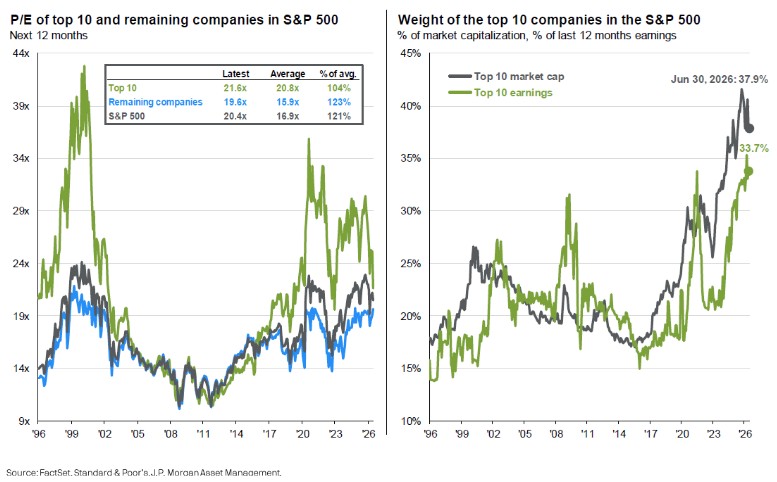

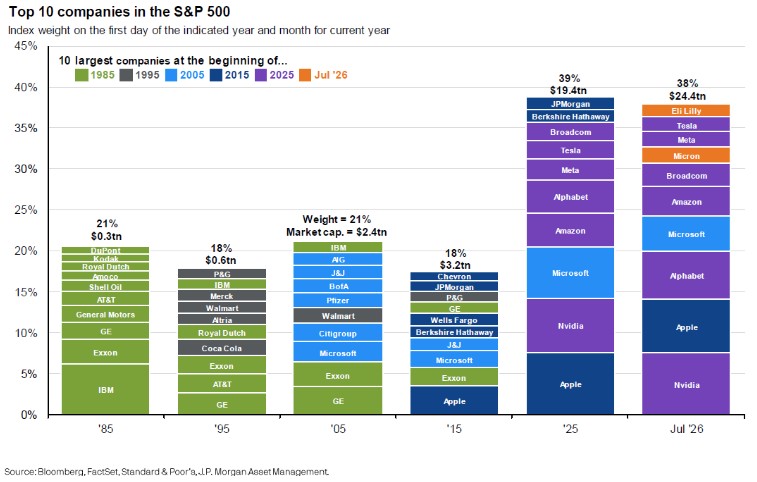

The 10 largest companies in the S&P 500 now account for 37.9% of the index’s market capitalization but only 33.7% of its earnings, trading at a forward P/E of 21.6x versus 19.6x for the other 490 companies.

For the first time, that top 10 list includes a memory chipmaker: Micron, alongside Nvidia, Apple, Microsoft, Alphabet, Amazon, Meta, Tesla, Broadcom, and Eli Lilly. A company that spent most of the last decade as a commodity cyclical is now sitting at the table with the platform giants, and that seat was earned specifically because of the price dynamic described above.

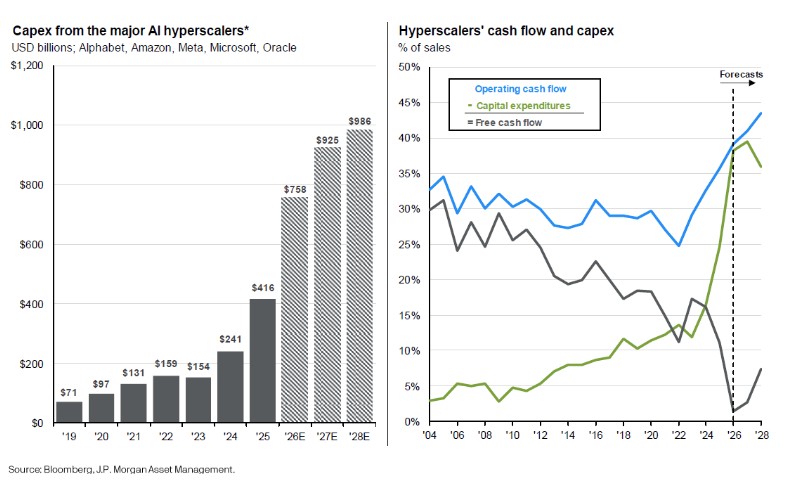

The earnings numbers explain why the market rewarded semiconductor stocks and punished hyperscaler stocks this quarter. Semiconductor earnings are projected to grow 103% in 2026, up from 53% in 2025, while hyperscaler earnings growth is decelerating, from 41% in 2023 to an estimated 28% in 2026. Semiconductors now trade at 22.5x forward earnings and represent 19.2% of the S&P 500. That is a very high bar to clear. Hyperscaler capital expenditures are projected to rise from $416 billion in 2025 to $758 billion in 2026, and to nearly $1 trillion by 2028 (p. 24), and that spending is the direct source of semiconductor demand. But memory chips are a direct line item in that spend, and a 200% cost increase on a core input does not disappear. It remains to be seen whether Hyperscaler will be able to increase prices or cut other expenses enough to maintain their profit margins.

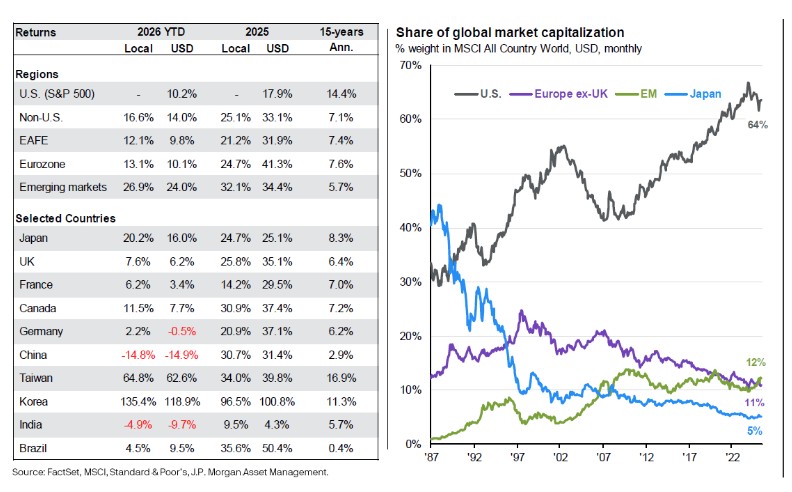

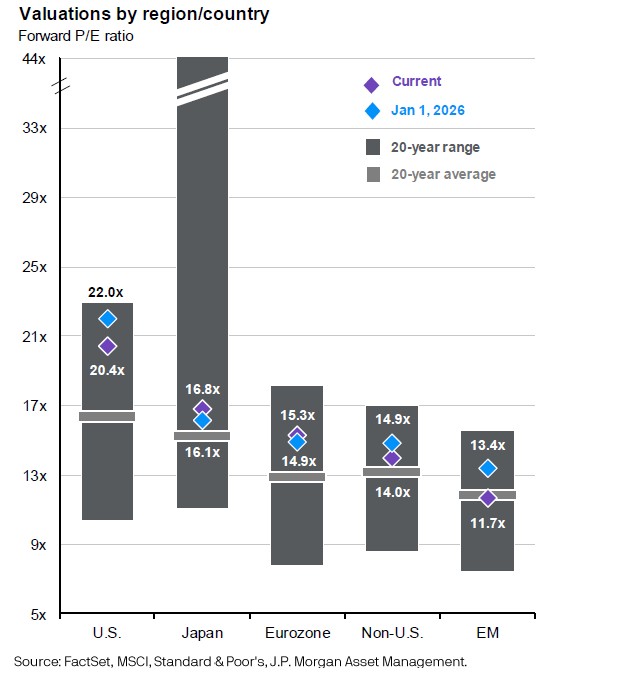

International markets offered a reminder that the U.S. does not have a monopoly on returns. Non-U.S. equities are up 14.0% year to date versus 10.2% for the S&P 500, and emerging markets are up 24.0% (p. 43). Non-U.S. developed and emerging market equities continue to trade at a meaningful discount to the U.S., 31% below on a forward P/E basis versus a 20-year average discount of 20% (p. 46). Fixed income remains a reasonable ballast, with the U.S. Aggregate yielding 4.73%, up from 4.32% at year-end (p. 36).

One thing I’m watching

The mechanism I’m watching closely is a System 2 problem hiding behind a System 1 rally. Semiconductor earnings are priced for 103% growth in 2026, and that estimate assumes hyperscaler capital spending keeps accelerating at its current pace. But hyperscaler earnings growth has already decelerated from 41% in 2023 to an estimated 28% this year, and hyperscaler stocks are down 5% year to date, which tells me the market already has some doubt about how long that spending pace holds. Memory chips are the mechanism that could resolve that doubt in the wrong direction. If DRAM and NAND prices keep climbing at anything close to the pace of the past twelve months, hyperscalers face a real choice: absorb the cost through compressed margins, which slows the capex growth semiconductor earnings are counting on, or pass it through to customers, which raises the cost of the very AI services meant to justify all of this spending. Either path makes a 103% earnings estimate harder to hit. This is not a call to abandon technology exposure. It is a reason to ensure that exposure is diversified across the supply chain, including the companies that make the chips, and not concentrated solely in the platforms that consume them.

What this means for your accounts

Nothing about this quarter changes the shape of your plan. Diversification across large cap, international, and fixed income did its job when oil spiked in April and did its job again when it retreated. The memory chip story is a reminder of why we own the picks and shovels alongside the platforms, not a reason to chase either.

Your Market Analyst,

Tony